.

Business conditions in Dubai recorded a faster rate of improvement as jobs and inventory growth reached multi-year highs in March, underscoring the enduring investor appeal and confidence in the emirate’s economic resilience and growth prospects.

The headline purchasing managers index (PMI) rose to 55.5 in March, up from 54.1 in February and to the highest level in five months. The index signalled a sharp improvement in non-oil business conditions, with the uptick supported by stronger growth in output, employment and stocks of purchases, alongside tighter supply side conditions.

Dubai’s PMI reflected a pick-up in growth momentum towards the end of the first quarter with both employment and inventory levels recording stronger growth rates, reaching multi-year highs.

A confluence of positive factors including innovative government strategies, visa and business reforms, a dramatic boom in real estate sector, and increased FDI flow and investor appeal, have been propelling Dubai’s growth irrespective of global and geopolitical headwinds, economists said.

Dubai has rolled out a mammoth $8.7 trillion economic plan for the coming decade, aimed at turbocharging trade and foreign investment while reinforcing the emirate’s position as a sought-after global business hub. Dubai is on track to emerge as one of the top four global financial centres with an increase in FDI to Dh650 billion as over 300,000 global investors are helping build Dubai into the fastest growing global city. The UAE economy, the Arab World’s second-biggest, is forecast to grow at 3.3 per cent in 2023, according to the latest World Bank report.

“The Dubai PMI picked up for the first time in three months in March as companies reported greater efforts to build supply-side strength in light of a further rapid expansion in activity levels,” said David Owen, senior economist at S&P Global Market Intelligence.

He said the rapid expansion and subsequent increases in staffing levels and inventories of materials and components were the sharpest seen in around five years, allowing firms to increase their output to the greatest extent for six months.

“However, a further slowdown in new business growth shows that demand growth is continuing to weaken from its post-Covid peak, with notable slippage seen in the wholesale and retail and travel and tourism sectors. This suggests that rapid activity growth may not be sustained, which was reflected in a slight drop in future output expectations,” said Owen.

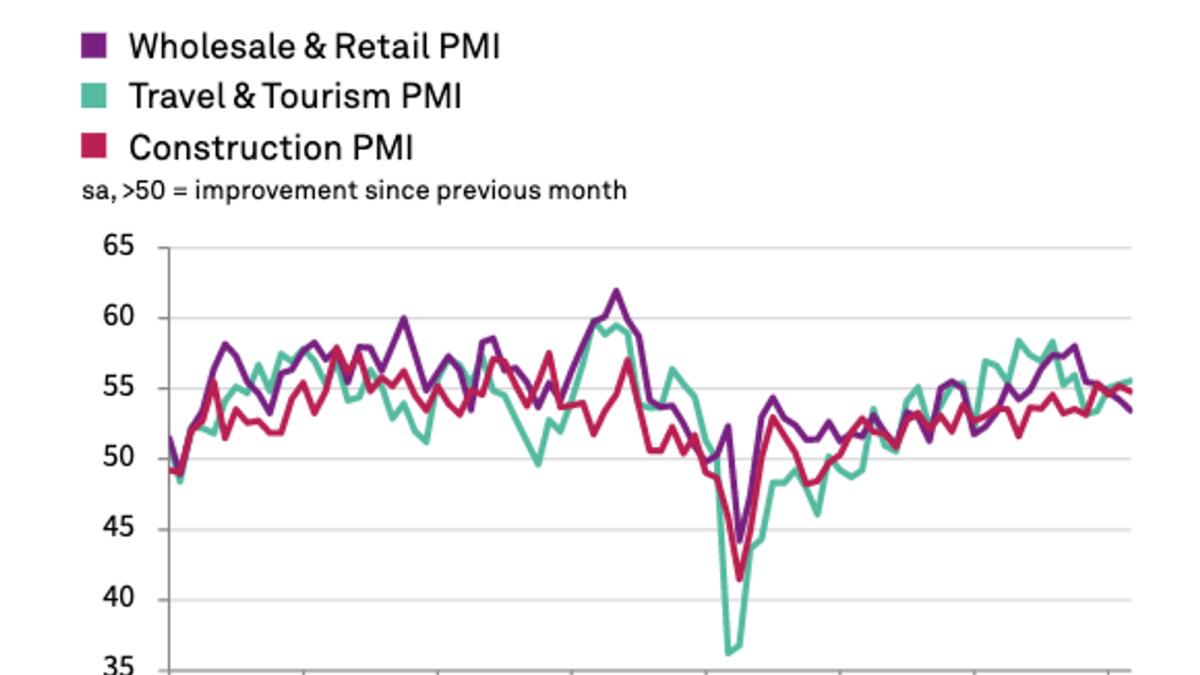

During March, Dubai companies continued to report a marked improvement in client demand as firms placed greater emphasis on building capacity levels to support an expansion in output, resulting in a substantial increase in activity that was the sharpest since last September, according to S&P Global Dubai PMI survey that covers the Dubai non-oil private sector economy, with additional sector data published for travel and tourism, wholesale and retail and construction.

New business inflows also increased sharply, although the rate of expansion eased slightly from February and was the least marked in just over a year. Sector data indicated that the wholesale & retail and travel & tourism sectors had lost momentum from their post-Covid peaks in 2022, with sales growth in the former reaching a 14-month low.

However, a sharp rise in output meant that firms had a greater need to expand their business capacity in March. Job levels subsequently rose, with the pace of job creation picking up to the fastest since January 2018, though still an increase in employment.

The March PMI data signalled an additional increase in input prices during March. Survey panelists noted rises in the price of fuel, cement and iron, as well as a slight uptick in staff wages.